Greedy doctors, overpaid agents, or kiasu patients? What is wrong with Integrated Plans?

One of the mysteries about insurance in Singapore is why the insurers providing Integrated Plans are not more profitable. Integrated Plans are Hospitalization and Surgery (H&S) plans complementing the Government-subsidized Medishield Life Plans (for B2 and C class wards at public hospitals) which give policy-holders access to B1 and A class wards at public hospitals and private hospitals. Is it a case of greedy doctors demanding to be paid more? Or is it a case of overpaid financial advisors and insurance agents who are churning customers for more commission? Or perhaps the fault lies in the kiasu mentality of the patients, who demand as much healthcare as the plans will cover them for?

Integrated Plans: A Short History

Rewinding back a few years, it wasn’t always this way. In fact, when private Shield Plans were first introduced back in 2005, they made profits for the insurers for more often than not for 10 years. After all, Singaporeans were getting rich fast, and demanded the best standards in healthcare. And it helped that these plans could be paid from Medisave. The financial advisory industry had just been restructured and liberalized, allowing much more competition in selling such policies. And while the population was ageing, the target audience for these plans were generally younger, and had less need to claim from these policies.

Underwriting Profits and Losses for Integrated Plans (2005 – 2016)

But all that seemed to have changed after the introduction of Medishield Life in 2015, as claims ratios soared, pushing all the insurers into the red.

Claims Ratios for Integrated Plans (2005 – 2016)

Only recently have some insurers been able to claw themselves back into profitability, in 2018 and in 2019.

Why are Integrated Plans Unprofitable?

But what has been the root cause of this unusual state of affairs? After all, the proportion of Singaporeans with Integrated Plans has gone up from just 19% in 2011, to 32% in 2015, and an astounding 66% in 2020! Astounding, because with 66% of the population entitled to make an insurance claim for a stay in public hospital A class wards or private hospital wards, there simply are not enough hospital beds to cater to them all!

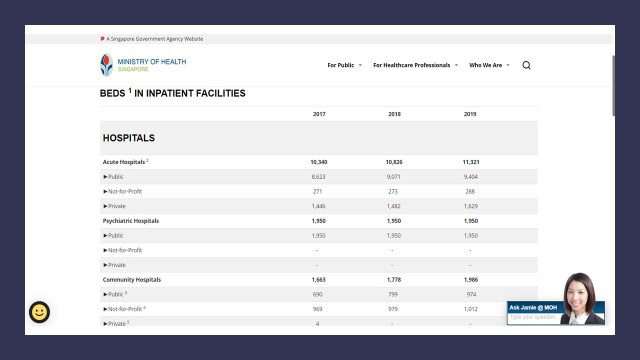

Hospital Beds in Singapore (2017-2019)

Private hospitals account for only about 15% of all the beds in acute hospitals, and the A class and B1 class wards in public hospitals probably account for another 15% to 20%. And it is not like we have beds to spare, since Singapore only has around 2 hospital beds per 1,000 people, which is way below Japan’s 13 beds, South Korea’s 12 beds, Germany’s 8 beds and even China’s 4 beds per 1,000 people! Hence, the likelihood of a successful claim is low, as only about half of the Integrated Plan policyholders would be able to claim on the plan. In all likelihood, despite having an Integrated Plan, they will more likely be making a claim on the base Medishield Life plan instead. All the more profitable for the insurers!

The usual suspects to blame for this current lack of profitability then fall on the greedy doctors, and kiasu patients. Ask any expert on this and this seems to be the usual response (here and here).

Doctors, because after having put in years of study to qualify as medical practitioners, demand to earn a living as good as their less educated classmates in banking and technology. Anyone who has visited a specialist in the past few years will know of the endless battery of tests and scans which doctors recommend in order to chase down every last dot and shadow on the X-ray or ultrasound or MRI scan. All of which are charged to the patient and insurer.

And patients with the buffet syndrome. Since Medishield Life and the Integrated Plan insurer are there to cover the medical bills (especially if the policyholder has a rider which covers the deductibles and co-payments), why not do as many tests and scans and operations as possible, and claim as much as they can?

But more recently, it has been opined that the commissions paid to financial advisers and the management costs are also to blame (see here and the response here). So who is right, and who is wrong?

How did the Integrated Plan Insurers Do in 2019?

Let’s look at how the Integrated Plan insurers did financially in 2019 (the latest year) for which their results are available to figure this out! Firstly, looking at the net premiums collected, we can see that there is a two tier market for Integrated Plans in Singapore, with four large insurers (Prudential, NTUC Income, AIA and Great Eastern) and a bunch of smaller ones. This indicates that we should consider these two groups of insurers separately, as there are definitely economies of scale at work in the insurance business.

Premiums Earned for Integrated Plans in 2019

| Insurer | Premiums Earned in 2019 |

|---|---|

| Prudential | $456 million |

| NTUC Income | $437 million |

| AIA | $341 million |

| Great Eastern | $321 million |

| AVIVA | $188 million |

| AXA | $54 million |

Now, let’s take a look at the various financial metrics of the underwriting business for Integrated Plans:

Underwriting Results for Integrated Plans in 2019 (% of Premiums Earned)

| Insurer | Claims Ratio | Management Cost | Distribution Cost |

|---|---|---|---|

| Prudential | 71% | 5% | 13% |

| NTUC Income | 83% | 9% | 7% |

| AIA | 69% | 12% | 19% |

| AVIVA | 80% | 13% | 12% |

| Great Eastern | 88% | 10% | 20% |

| AXA | 65% | 32% | 37% |

Financial Results for Integrated Plans in 2019 (% of Premiums Earned)

| Insurer | Underwriting Result | Net Investment Income | Operating Results |

|---|---|---|---|

| Prudential | 11% | 0% | 11% |

| NTUC Income | 1% | 9% | 10% |

| AIA | 0% | 2% | 2% |

| Great Eastern | -18% | 5% | -13% |

| AVIVA | -5% | 1% | -4% |

| AXA | -34% | 2% | -32% |

So what can we learn from the 2019 experience? There seem to be a few things to note when we realise that three of largest insurers have positive underwriting and operating results:

1. Scale Matters

Clearly, scale is something which affects the outcomes, and given the inexorable rise in population and in premiums over time, it is something that the insurers will achieve over time. Hence there is no need to take too much heed about how the Integrated Plan business is unsustainable. Moreover, since Singaporeans have a penchant for over insuring themselves heath-wise (there are more Integrated Plans as a proportion of population than A class and private ward hospital beds in acute hospitals), growth is of little concern.

2. Claims ratios – Neither doctors nor patients are greedy or kiasu

Secondly, it appears that despite all the protestations made earlier, the claims ratios are not really so high. After all, the biggest 3 are profitable despite having claims ratios in the range of 69% to 83%, which are as high as back in 2015 and 2016. So contrary to popular opinion, doctors are neither overly greedy nor are patients overly kiasu. The over-medication and buffet syndromes are probably more fiction than fact.

In fact, if we look at how the Affordable Care Act (ACA) or Obamacare is set up in the US, we see that it actually mandates that medical claims as a percentage of premiums have to be at least 80%! And for larger groups, they are to be at least 85%, to ensure that not too much of the premiums go into profits. In fact, if the insurers do not hit this level of claims, they need to rebate some of the premiums back to the policyholders.

Hence the claim that doctors are too greedy, and patients are too kiasu is simply a myth!

3. Management costs – Insurers are inefficient at processing claims

Next, looking at the Management Costs, it appears that the loss-making insurers are either just too small and inefficient in claims processing, or they are costing operational costs too highly (remember, they run other lines of business besides Integrated Plans). The less profitable insurers all run Management Costs of more than 10% of Premiums Earned.

While making a claim does involved some effort, because of the kiasu nature of the Integrated Plan policyholders, there is anecdotal evidence that many of the Integrated Plan claims are actually for the expenses at subsidised wards covered under Medishield Life, which means that the actual claims processing is done by the CPF! If the insurers are still racking up large Management Costs despite this, then they surely have themselves to blame only.

4. Distribution Costs – Advisors Commissions seem to high

Just like Management Costs, the Distribution Costs look fairly high for the insurers which are unprofitable. The most profitable Integrated Plan insurers have Distributions Costs managed between 7% to 13% of Premiums Earned, while the unprofitable ones have Distribution Costs ranging from 12% to 37% of Premiums Earned. Perhaps there is some truth that the insurers are paying the Financial Advisers and Insurance Agents too much in commissions, or that the structure of the commissions is not balanced, because the high turnover of the Financial Advisers and Agents in the industry mean that commissions are often paid by policyholders to someone who ultimately does not help service their policies when needed.

Another factor that could be driving up the Distribution Costs of Integrated Plans is the turnover of policies, as existing policyholders are persuaded to move over to another insurer by their Financial Advisers. After all, Hospitalization & Surgical policies are easier than General Insurance policies to sell and retain, as once the policyholders develop medical conditions, they cannot easily move their insurance cover to another insurer due to the exclusion of coverage for pre-existing conditions. And yet there is likely too much bargain hunting for the cheapest Shield Plan along with too few incentives for policyholders to stay put at their insurer whcih drives this outcome in Singapore.

There is some truth in the allegation that Management and Distribution Costs are too high for Integrated Plans

5. Net Investment Income – Strangely too low

Even if the insurer makes and underwriting loss (i.e. premiums earned minus claims, management and distribution costs), the insurer can still be profitable if the investment returns on the premiums earned are high enough. From the table above, the investment income ranged between 0% to 9% in 2019. Which seems very low indeed. Now, before someone says that this is because 2019 was a bad year for investments, 2019 was actually pretty good investment-wise.

And further note that the very same group of insurers (with the exception of Prudential) had Net Investment Income ranging between 3% to 23% for the General Insurance portfolios! After all, these are the same people who claim that they have the expertise to manage the investments in your Whole Life and Investment-Linked Life Insurance policies! We should definitely expect them to do better!

How does Integrated Plan Insurance compare to General Insurance?

To provide one further point of comparison, let’s look at the corresponding financial metrics of General Insurance in Singapore. The vast bulk of General Insurance in Singapore is Auto Insurance. Healthcare Insurance is quite similar to General Insurance in many ways.

For a start, both a short term yearly-renewable policies with relatively sort loss/claim triangles. Although Healthcare Insurance is usually touted as for the long term, most claims are settled within a couple of years from the time they are diagnosed or incurred, and the rising structure of premiums as the policyholder ages means that little of the premiums collected in any year needs to be put aside as reserves for future claims. And because of the specter of rising hospitalization and surgery costs, and pre-existing conditions, it should be easier to sell Healthcare Insurance policies and retain the policyholders over time, compared to General and Auto Insurance, where No-Claim Bonuses are fully portable across insurers.

Let’s take a look at the data:

Premiums Earned for General Insurance in 2019

| Insurer | Premiums Earned in 2019 |

|---|---|

| NTUC Income | $343 million |

| AIA | $16 million |

| AVIVA | $25 million |

| AXA | $306 million |

| Great Eastern | $66 million |

Now, for a start, General Insurance has smaller scale than the Integrated Plans, which means that scale should not matter so much as initial thought for profitability of the Integrated Plans.

Underwriting Results for General Insurance in 2019 (% of Premiums Earned)

| Insurer | Claims Ratio | Management Cost | Distribution Cost |

|---|---|---|---|

| NTUC Income | 60% | 19% | 18% |

| AIA | 24% | 18% | 37% |

| AVIVA | 76% | 32% | 7% |

| AXA | 60% | 22% | 22% |

| Great Eastern | 51% | 29% | 10% |

Financial Results for General Insurance in 2019 (% of Premiums Earned)

| Insurer | Underwriting Result | Net Investment Income | Operating Results |

|---|---|---|---|

| NTUC Income | 4% | 23% | 27% |

| AIA | 21% | 19% | 39% |

| AVIVA | -15% | 3% | -11% |

| AXA | -4% | 11% | 7% |

| Great Eastern | 10% | 8% | 18% |

Looking at the results for General Insurance in 2019, and comparing them to Integrated plans, we see that:

- General Insurance has lower Claim Ratios …

- … but higher Management and Distribution Costs, which makes sense because all the claims are processed by the insurer, and it is harder to retain customers from year-to-year

- Investment Income is also higher …

- … which helps to turn border line underwriting losses into solid operating profits in most cases

So, the question clearly is that the insurers tend to be able to manage their General Insurance operations profitably. Why can’t they do the same for Integrated Plans?

Conclusion: Doctors aren’t quite as greedy, nor are patients quite as kiasu as what we’ve been told

So despite all we’ve been told about how doctors are trying to charge more, and how patients with the buffet syndrome are claiming more, the low profitability of insurers offering Integrated Plans does not really seem to be due to claims. In fact, it is a combination of high Management Costs, high Distribution Costs and low Investment Income which are the causes of poor profitability for Integrated Plans. The financial figures also show that the insurers which have a better handle on these three financial items are the ones which are the most profitable.

Of course, this does not mean that spiraling healthcare charges from hospitals and doctors, and rising claims from patients will not ultimately create issues with the sustainability of healthcare insurance. But that has not been the story of the past few years for the Integrated Plans. Hence, it’s time to give that standard narrative of “Greedy Doctors and Kiasu Patients” a rest.

It’s time to give that standard narrative of “Greedy Doctors and Kiasu Patients” a rest

*Here is the much awaited follow up on this post with more details!

10 thoughts on “Greedy doctors, overpaid agents, or kiasu patients? What is wrong with Integrated Plans?”